Preparedness

hey~ I don’t need LIFE INSURANCE!

“A man who dies without adequate Life insurance should have to come back and see the mess he created!” Will Rogers

There are so many reasons why people buy Life insurance. But, in the real world we always try to find the easier way out of a situation. We know what the situation kinda’ looks like but we don’t know the impact it will make or not make in the outcome. We avoid another bill, or another monthly payment to our ever increasing list of commitments, budget and expenses you can’t live without. Definitely we will analyze in our minds how we don’t want the extra premium in our monthly expenses, hey I’m right there with ya’! But, instead we really need to look at what if? What if something did happen, we know it will so why not look at the idea of what plan suits us best. Both for our needs and our budget.

The big question is of course, well how much do I need and for how long.

Especially when money is tight, our budget doesn’t allow the extra costs especially now during Covid19, or any other event that occurs in our life. But planning doesn’t stop. Just because your budget doesn’t need any extra expenses in it, our lives don’t stop. You don’t stop the clock, the clock keeps turning, it keeps ticking. What does that mean? It means that we don’t have choices on planning our health, our sicknesses, our disabilities, our accidents, our life-changing events. But we do have control in planning for our future as well as those around us. What does that look like? I always start with how much can I fit into my budget? What will be comfortable to handle even in the hard difficult times?

When you don’t have your own personally owned life insurance policy you have the risk of losing it, not having control of the coverage or the exclusions, and length of time you wish to have it for. So, putting it bluntly, you don’t have control over it at all. Especially important when you aren’t as healthy as you used to be!

This Blog is relatively consistent in most countries but you will need to use your knowledge that you learn from the Blog to how it works in your own country to what is available.

Now remember that you don’t have an medically underwritten personally -owned policy, there are no guarantees.

MORTGAGE INSURANCE: is not personally owned policies and is not medically underwritten. Sometimes there are medical testing done, but they don’t look at the complete underwriting process as do personally-owned policies. They are normally policies that are underwritten at the time of death. Which can create issues when making your claim. Check out this video on Mortgage insurance policies.

What can a Life insurance policy do for you and your family?

Things to consider what you want Life insurance to do for you and your family.

- Cover funeral, burial expenses

- Help to replace lost income

- Help pay off the mortgage

- Leave somethin’ somethin’ for those you leave behind

- Giving to your favourite charity

- Even leave some behind for who is looking after your children

- Blended partnerships to make it equal on both sides so no one side is left without anything

- Income tax advantages

Be careful in knowing what insurance does what on death. Because they are not all the same. And that’s why we usually keep buying more and more and more from any agent that we come across because we don’t know what’s what! So hopefully in our YOUR BACKUP PLAN BLUEPRINT, you will be a pro when we will go over policies and what they are and how they work.

How to join YOUR BACKUP PLAN BLUEPRINT? The link will be available soon for a complete library of videos with step by step guides, how to videos, worksheets and interviews on why you should do it. Why? Because now you have the understanding, the knowledge, and the custom plan for you and your family in case of any circumstance.

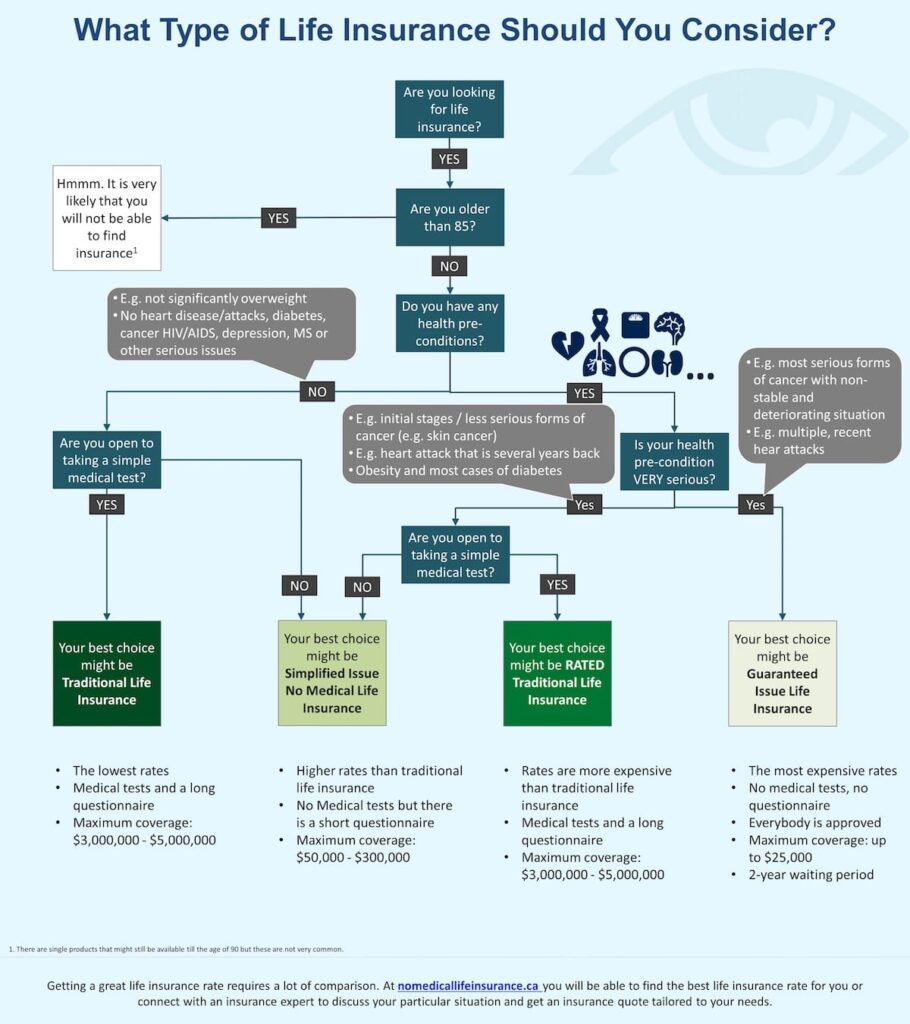

DIFFERENT TYPES OF INSURANCE

So looking at any of all of the options that are available out there is passing the first question:

- How old are you? Under age 85?

- Do you have any health issues that would prevent you from completing a Medical test?

- What do you want the coverage for?

The rest is easy smeezy! As long as you qualify with a medical test your options are endless! Especially with saving money buying a policy as well as health wise you may have some companies offer you lower rates! Wow! Right? So the above questions are really where you need to start.

The amount of coverage really doesn’t matter because if you don’t qualify health wise then you only have 1 or 2 other options and they are not cheap. No medical test policies- or Guaranteed Issue are usually the most expensive way of buying life insurance. Because for the Insurance company it is the biggest risk to be able to pay off the claim when needed.

So by planning ahead when you are healthy, you can then take a simple medical test, and then decide how much you would like as well as the premium that you can afford to look after.

You will have the choice of Medically underwritten life insurance policies or Guaranteed issued policies. What are the differences?

Medically underwritten Policies once approved, and paid on time consistently, the insurance company is bound by the contract. Underwritten policies will normally have a 2 year suicide clause included but you would be covered for anything that happens in your life as well as anything after the 2-year window. Why? Because it is medically underwritten, approved and you pay for the policy to keep it active. Non-medically approved policies usually have a large number of exceptions to them. You may not be covered if you were to pass away from cancer or a stroke, as an example. You have to read the fine print of exceptions. Insurance companies cannot afford to take the risk with your policy if you aren’t underwritten.

What types of things do Underwriters consider?

Underwriters consider the following things:

- Your close immediate family’s health, mother, father, sister and brother under the age of 80.

- Your current and past history of drug use

- Saliva test

- Smoking usage

- Your own medical tests which could consist of blood work, urine, weight/height and blood pressure as ordered by the insurance company

- They will need a list of current prescriptions

- The insurance company will then look at your past medical that is on file

- The insurance company may also contact your doctor for a report as well

Occassionally all of these considerations are not all used but 1 or all could be used for the Underwriters if they choose to do so.

Sometimes, when the insurance company contacts your doctor for more answers or to understand a person’s condition they will order a doctor’s report. A lot of people then get worried but you don’t have anything to worry about. Why? Because they can find out what the risk is involved in that specific condition once the doctor gives them better clarity. Once approved you will never have to be approved again as long as you continue to pay your premiums and keep it active.

You can look at TERM Life insurance.

Term Life insurance

Term insurance is a type of policy that provides coverage for a certain period of time or a specified “term” of years. Only by years no months!

When the insured person passes away during the specified term or time period of the policy and the policy continues to be active or in force there will be a specified death benefit to your beneficiary as in the policy details.

Term insurance is initially much less expensive when compared to a Permanent Life insurance policy- because they have an END date. Term insurance have no guaranteed cash value because the guarantee with term insurance is the guaranteed death benefit to your beneficiary. You can extend the policy longer guaranteed if you wish to. But the cost will be stipulated at the age you are making the changes on. No further medical tests will be required because you have an active life insurance policy, you are only converting it at that point. The length of Term insurance is normally 10 year, 20 year, 30 year and 40 years. So, my favourite is either layering Term insurance with different terms. So as an example, you could have $500,000 for the first 20 years and then the next 10 year window $400,000 and then the last 10 year window you would have $200,000. So this is an idea of a complete look at the whole length of your life coverages. You may be 30 years old and this plan would look like $500,000 until age 50 then you would $400,000 to age 60 and then $200,000 until age 70. Looking at anything beyond age 70, it would be more economical for you to consider another layer with permanent option for the part past 70 yrs old.

Permanent Life insurance

The options for a permanent Life insurance policy are the following:

- Whole Life

- Universal Life

The biggest difference with a permanent policy is that it doesn’t have an end date or a termination of the policy. It doesn’t matter how old you get because there is no end date. With both of these policies you have the benefit of the guaranteed death benefit, and a savings component where cash value will accumulate. You can choose in many cases to your fund that you wish to use for accumulation. You can choose who you wish to pass the cash component of the policy to as well as the insurance component. The cash component and the death benefit will transfer tax free to a designated beneficiary. In both of the policies, you either receive a guaranteed death benefit or a guaranteed amount of funds in your policy by a certain date. Most policies allow you to withdraw the cash funds or some of them but still keep the policy in tact. The cash value of these policies are nice because you can sometimes use the cash value to pay the policy when you have retired, or you can withdraw some of it for renovations, travel, pay off your mortgage or something exciting! Or you can use the cash value as a transport vehicle to your beneficiary tax-free.

My ideal combination of some term and some permanent life insurance is layering it so you have more coverage when you really need it, working with bigger mortgage amounts and bigger income loss. Layering a few term policies with a permanent option is the most ideal coverage. The layering allows you be insured that you have a certain amount for a death benefit at certain years in your life when you need it higher and then less when you don’t need as much. And the best part is the costs continually goes down even when you are getting older! What??? that’s right. The cost, the premiums continually decrease for you as you enter retirement! You can’t get much better than that, can you?

So do you need Life insurance? Something you control, something that is there when you need it the most, and the premiums can be regulated as you wish it to look like, and they go continually decrease over the years! Imagine that!

Oh dear!! I could write on this topic forever and forever!

Enjoy our fun PODCAST SHOW this week with Jarrod Merkel, from Merk Financial Group in Vancouver, BC. I hope you can learn a few tips and tricks to get your plan and understand what you already have.

Related posts

Preparedness

THE MORE OBSTACLES I OVERCOME THE STRONGER I BECOME

“The more obstacles I overcome, the stronger I become”, Gracie Alvarez David is an award-winning…

Preparedness

I’VE GOT TO BEAT THIS TRAUMA IN MY LIFE!

“The more obstacles I overcome, the stronger I become”, Gracie Alvarez- I’VE GOT TO BEAT…

Preparedness

CLINICALLY DEAD A DOZEN TIMES

“Sometimes a little near death experience helps them put things into perspective”, Anne Shropshire Our…

Preparedness

TIPS TO HELP YOU MOVE FORWARD

TIPS TO HELP YOU MOVE FORWARD AFTER METASTATIC BREAST CANCER “Courage doesn’t always roar. Sometimes…

{kind=link}

Preparedness

SHIFT HAPPENS WHEN ….

Shift Happens when …… we can experience the change, it hurts and maybe uncomfortable but…

Comments are closed

Share Your Thoughts